company registration india

( One person company, private limited company, public limited company, limited liability partnership, FCRA, Nidhi Limited Company)

Call us @ +91-8800-100-284

Call us @ +91-8800-100-284

|

This guide is all about two key asset of a company Share & Stock. What is Share and Stock of a company, and what are the main differences between share and stock of a company. It is a Must read while going for Company Registration in India. Share and Stock are key elements of a company, but in general most people think that there is no difference between Share and Stock, We bring here highlighted differences between these two important key assets of company. Know here what is Share of a company and what Stock of a company is, and Get classified information on differences between Share and Stock. Share: - A Share is single unit that is used as a measure of various investments in financial markets or a company. Share is used in collective investments such as Mutual Funds, Limited Partnerships, and Real Estate Investment Trusts. Owner of a share is called Shareholder, every share has some face value, and this face value is an agreement to the Shareholder that Company will pay the face value of share to the shareholder when he sells his share. Stock: - Stock is also a Share; Stock is a share in ownership of a company. If you have a stock of a company means you are one of the many owners of that company. You are the owner of all company assets whether that is furniture, or trademark, or contract of the company. Having a stock of company says that you are a partner of company in all earnings, in all benefits, in voting rights, and in all lost. Here below are the Major differences between Share and Stock of a Company, check here:

These are the major distinction points that to be considered while studying the differences of Shares and Stocks.

Get services of Company Registration and Trademark Services in India from Top Lawyers of Company Law and IPR in India. Anita Aswal (Company Secretary) +91-8800-100-284 [email protected] S-191C, Manak Complex, School Block, Shakarpur, New Delhi, 110092

15 Comments

One Person Company Advantages The privileges and exemptions enjoyed by a one person company or its advantages over other companies are as follows:

Company-Registration-India Paid up capital/turn-over of One Person Company not to exceed prescribed limits

When the paid up share capital of an One Person Company exceeds fifty lakh rupees or its average annual turnover during the relevant period exceeds two crore rupees, it shall cease to be entitled to continue as a One Person Company. One Person Company to convert itself on exceeding the above limits One Person Company where the paid up capital/turnover as the case may be exceeds the prescribed limits, shall be required to convert itself, within six months of the date on which its paid up share capital is increased beyond fifty lakh rupees or the last day of the relevant period during which its average annual turnover exceeds two crore rupees as the case may be, into either a private company with minimum of two members and two directors or a public company with at least of seven members and three directors in accordance with the provisions of section 18 of the Act. Alteration of Memorandum and Articles The One Person Company shall alter its memorandum and articles by passing a resolution to give effect to the conversion and to make necessary changes incidental thereto. Notice to Registrar The One Person Company shall within period of sixty days from the date of applicability, give a notice to the Registrar in Form No.INC.5 informing that it has ceased to be a One Person Company and that it is now required to convert itself into a private company or a public company by virtue of its paid up share capital or average annual turnover, having exceeded the threshold limit. Penalty for default If One Person Company or any officer of the One Person Company contravenes the provisions of these rules, One Person Company or any officer of the One Person Company shall be punishable with fine which may extend to ten thousand rupees and with a further fine which may extend to one thousand rupees for every day after the first during which such contravention continues. Minimum number of members/directors/ capital to be complied on conversation A One Person company can get itself converted into a Private or Public company after increasing the minimum number of members and directors to two or minimum of seven members and two or three directors as the case may be, and by maintaining the minimum paid-up capital as per requirements of the Act for such class of company and by making due compliance of section 18 of the Act for conversion of companies already registered. Distinction between Memorandum of Article (MOA) & Articles of Association (AOA): MOA v/s AOA8/30/2016  Company-Registration-India: MOA vs AOA MOA v/s AOA, Explained below are the key differences between MOA & AOA. Explore below The main points of Distinction between Memorandum of Articles and Articles of Associations:

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Passed in Lok Sabha

|

December 18, 2012

|

|

Passed in Rajya Sabha

|

August 08, 2013

|

|

President’s assent

|

August 29, 2013

|

|

Total number of sections

|

470

|

|

Total number of chapters

|

29

|

|

Total number of schedules

|

7

|

|

Number of sections notifies (282)

|

Section 1 on August 29, 2013

98 sections on September 12, 2013 183 sections on April 01, 2014 |

|

Total number of rules notified

|

Rules under 21 chapters notified

183 sections on April 01, 2014 |

| articles_of_association_of_a_company_limited_by_guarantee_and_not_having_share_capital.docx |

| articles_of_association_of_a_company_limited_by_guarantee_and_having_a_share_capital.docx |

| articles_of_association_of_a_company_limited_by_shares.docx |

| articles_of_association_of_an_unlimited_company_and_having_a_share_capital.docx |

| articles_of_association_of_an_unlimited_company_and_not_having_share_capital.docx |

Serial Number |

New e-form (Sample) |

What is the Purpose of Application Form? |

1 |

Application For Reservation of Company Name |

|

2 |

Application Form for One Person Company (OPC) Incorporation |

|

3 |

One Person Company (OPC)- nominee consent forms |

|

4 |

One Person Company (OPC)- Change in Members/Nominees |

|

5 |

One Person Company (OPC)- Intimation of Cessation |

|

6 |

One Person Company (OPC)- Application for Conversion |

|

7 |

Incorporation for Conversions (Other than Companies) |

|

8 |

Application to Regional Director for Conversion of Sec.8 Company into any other type of Company |

|

9 |

Intimation to Registrar for Revocation, Surrender of License Issued under Sec 8 |

|

10 |

Application for Commencement of Business |

|

11 |

Notice of Situation or Change of Situation of Registered Office |

|

12 |

Application to Regional Director for Approval to Shift the Registered Office from One State to Another State or from Jurisdiction of One Registrar to Another in the Same State |

|

13 |

Application for Change of Name |

|

14 |

Conversion from Private to Public and Vice Versa |

|

15 |

Notice of Order of the Court or Tribunal Any Other Competent Authority |

|

16 |

Return of Allotment |

|

17 |

Notice to Registrar for Alteration of Share Capital |

|

18 |

Letter of Offer |

|

19 |

Return in Respect of Buyback of Securities |

|

20 |

Application for Registration of Modification or Creation of Charge ( Other Than Debentures) |

|

21 |

Particulars of Satisfaction of Charge |

|

22 |

Notice of Appointment or Cessation of Receiver or Manager |

|

23 |

Application for Registration of Creation or Modification of Charge in Case of Debenture |

|

24 |

Filling of Resolutions and Agreements to Registrar Under Sec-117 |

|

25 |

Application for Allotment of Director Identification Number (DIN) |

|

26 |

Intimation of Change in Particulars of Directors to be given to Central Government |

|

27 |

Notice of Resignation of Director to the Registrar |

|

28 |

Particulars of Appointment of Directors and the Key Managerial Person and the Changes Among Them |

|

29 |

Return of Appointment of Managing Director, Whole Time Director or Manager |

|

30 |

Form of Application to the Central Government for Approval of Appointment or Reappointment and Remuneration or Increase in Remuneration or Waiver for Excess or Over Payment to Managing Director or Whole Time Director or Manager and Commission and Remuneration to Directors |

|

31 |

Application by a Company for Registration Under Sec-366 |

|

32 |

Information to be Filed by Foreign Company |

|

33 |

Return of Alteration in the Documents Filed for Registration by a Foreign Company |

|

34 |

List of all Principle Place of Business in India Established by Foreign Company |

|

35 |

Annual Return |

|

36 |

Memorandum of Appeal |

|

37 |

Application to ROC for Obtaining the Status of Dormant Company |

|

38 |

Return of Dormant Company |

|

39 |

Application for Seeking Status of Active Company |

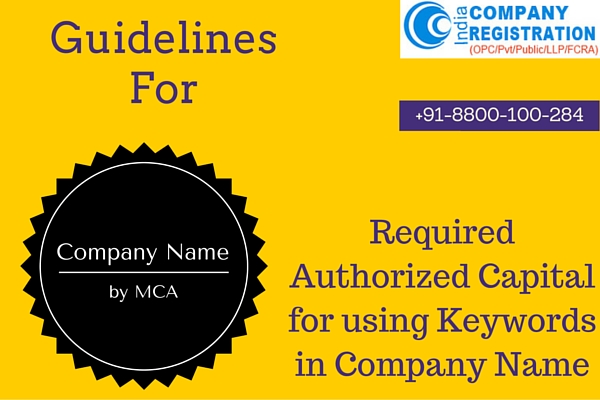

Key Words in the Name of a company |

Authorized Capital Required (INR) |

Corporation |

5 Crores |

International, Globe, Global, Universal, Universe, Continental, Inter-Continental, Asiatic, Asia, Asian, World being the first word of the name |

1 Crore |

If any of the key words at 2 above is used within the name (with or without brackets) |

50 lakhs |

Hindustan, Hindustani, Hindustanee, India, Indian, Bharat, Bhrarati, Bharatiya, Bharateeya, being the first word of the name |

50 lakhs |

If any of the key words at 4 above is used within the name (with or without brackets) |

5 Lakhs |

Industries / Udyog / industrial, industry |

1 Crore |

Enterprises, Enterprise, products, product, Business, Manufacturing, manufacture |

10 lakhs |

5/2/2016

Taxes or Remunerations |

Private Limited Company |

Limited Liability Partnership |

Applicability of Surcharge |

Applicable if Taxable Income exceeds to 1 Cr. During Financial Year |

Not Applicable |

Dividend Distribution Tax |

Applicable as Current DDT Rate of 16.2225 % |

Not Applicable |

Loan to Director or Partner |

Treated as DDT (Dividend Distribution Tax) |

Not Taxable as Income |

Expenditure for Family Planning |

Cannot be Claimed |

Can be Claimed |

Remuneration to Partner or Director |

Remuneration can be paid with no maximum limit |

Remuneration can be paid with fixed Limit |

Minimum Alternate Tax (MAT) |

a. If Taxable Income Exceeds 1 Crore : 20.0077% b. If Taxable Income Below 1 Crore : 19.055% |

a. If Taxable Income Exceeds 1 Crore : 19.055% b. If Taxable Income Below 1 Crore : 19.055% |

Normal Tax |

a. If Taxable Income Exceeds 1 Crore : 32.445% b. If Taxable Income Below 1 Crore : 30.90% |

a. If Taxable Income Exceeds 1 Crore : 30.90%% b. If Taxable Income Below 1 Crore : 30.90% |

Wealth Tax |

Applicable as 1% |

Not Applicable |

Method of Accounting |

Mercantile System of accounting |

Cash accounting system cannot be applicable |

Audit |

Audit is mandatory for all companies whether they company have share capital or not |

Audit mandatory if turnover exceeds 40 Lacs or capital contribution more than 25 Lacs |

Section 79 for Carry Forward & Set Off Loses |

Section 79 Applicable subject to some conditions |

Section 79 not applicable |

In this blog post you will get all the most important information over company registration services and foreign direct investment.

All

Aoa

Articles Of Association

Companies In India

Company Act 2013

Company Incorporation Forms

Company Law

Company Registration In India Application Forms

Company Tax For Private Limited Company & Limited Liability Partnership (LLP)

Corporate Law In India

Definitions Related To Company

Doing Business In India

E-forms For Company Incorporation In India Based On Companies Act 2013

FDI In India

FDI Policy

Foreign Direct Investment

Guide For Company

Limited Liability Company Formation In India

Make In India

Minimum Alternate Tax (MAT) For Private Limited Company & Limited Liability Partnership (LLP)

One Person Company (OPC) In India

Policies And Documents For Small Business

Remuneration For Directors In Private Limited Company & Limited Liability Partnership (LLP)

Taxability Of Private Limited Company & Limited Liability Partnership (LLP)

Tax Audit For Private Limited Company & Limited Liability Partnership (LLP)

Tax Benefits For Private Limited Company

Tax Filing In Private Limited Company & Limited Liability Partnership (LLP)

Wealth Tax In India For Private Limited Company & Limited Liability Partnership (LLP)

What Is Articles Of Association (AOA) Of A Company?

RSS Feed

RSS Feed